Mortgage Interest Tax Deduction: What You Need to Know

Key Takeaways

- To claim the mortgage interest tax deduction, homeowners must be legally liable for the debt on a qualified primary or secondary residence, itemize deductions on IRS Form 1040, Schedule A, and reference the interest reported on Form 1098 by their lender.

- The IRS distinguishes between acquisition indebtedness (funds used to buy, build, or substantially improve a home) which is capped at $1 million ($500,000 if married filing separately), and equity indebtedness (home equity debt used for other purposes) which is limited to $100,000.

- When refinancing a mortgage to secure a lower interest rate or extract equity, homeowners typically incur closing costs of 3% to 6% of the loan amount; these costs are often tax-deductible, though generally amortized over the life of the new loan rather than deducted fully in the year of refinancing.

- Utilizing a second mortgage or a Home Equity Line of Credit (HELOC) allows homeowners to tap into accumulated home equity, with HELOC interest deductions being strictly contingent upon the actual balance borrowed and utilized during the tax year.

One of the best justifications for owning a home, at least for financial reasons, is the tax savings that result from deducting mortgage interest. The deduction for mortgage interest stands as one of the few remaining tax deductions for the typical middle-class taxpayer.

Despite the changes to the tax code over the years and the repeal and limitation of many non-housing itemized deductions, mortgage interest is still deductible. On first and second mortgages and home equity lines of credit (with some limitations) for first and second homes, your mortgage interest deduction is still a good financial incentive to buy a home.

Mortgage interest deductions

What counts as mortgage interest?

Under the current tax code, mortgage interest on first and second homes is generally deductible as long as these loans total less than $1 million ($500,000 or less if married filing separately), making homeownership one of the best ways to trim your tax bill. You have to be legally liable for the debt (meaning your name is on the mortgage) and itemize your deductions on Form 1040, Schedule A to claim mortgage interest. Keep in mind, if the loan is not a secured debt on your home*, it is considered a personal loan, and the interest you pay usually isn't deductible.

*A home is defined by the IRS as “a house, condominium, cooperative, mobile home, house trailer, boat, or similar property that has sleeping, cooking, and toilet facilities.”

You should receive a Form 1098, a Mortgage Interest Statement, from your mortgage lender at the beginning of the new tax year. This form reports the total interest you paid during the previous year.

Types of mortgage debt

There are two different kinds of debt.

1. The money you borrow to buy, build or substantially improve your residence is called "acquisition indebtedness" or “home acquisition debt.”

2. The money you borrow against the equity in your home, or money you take out when you refinance your home for any reason except home improvement, is called "equity indebtedness" or “home equity debt.”

Loans that are exempt

When you borrowed the money is also important. Home loans taken out before October 14, 1987, are exempted from some rules. You may fully deduct interest paid on these loans, regardless of their size or what you used them for. Any refinanced debt you incurred before October 14, 1987, is rolled into your total acquisition indebtedness.

On loans made on or after October 14, 1987, you can deduct mortgage interest paid on acquisition indebtedness up to a total of $1 million ($500,000 or less if married filing separately). This means you could buy a home for $250,000, a beach home for $200,000, and add a family room to your first house for another $100,000, and still have $450,000 to spend on these homes for further improvements before you reached your limit for interest deductibility. The $1 million is not cumulative.

Your equity indebtedness (home equity debt) limit is $100,000. That means that you can borrow up to $100,000 of the equity in your home and use it for whatever you want. This is a change from the pre-1986 tax rule that limited your equity borrowing beyond the purchase price to certain qualified expenses, such as home improvements, medical and education expenses.

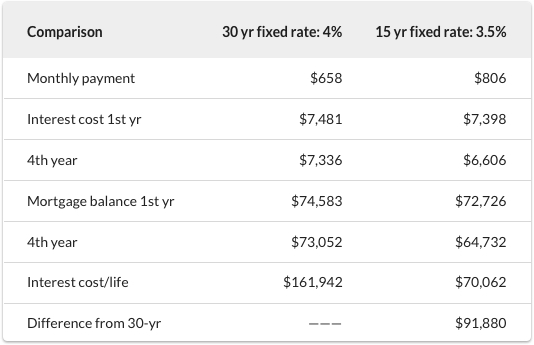

Refinancing your mortgage

Interest rates remain low, and because of that many homeowners have taken advantage of mortgage refinancing. Refinancing your mortgage continues to be an excellent opportunity to lower your interest rate, lower your monthly payment, or take equity out of your home.

When refinancing your mortgage, you will probably pay 3-6% of the loan amount in closing costs for surveys, legal fees, and paperwork fees. Many of these closing costs are deductible, but not necessarily in the year that you refinance.

Deducting interest paid

If you are considering refinancing your mortgage, there are a couple of things to bear in mind. If you refinanced before October 14, 1987, for a longer term than was remaining on the pre-October 14 loan, you may only deduct the interest paid on the mortgage for the term that was remaining on the old loan. So, if you refinanced a loan with 15 years remaining for a 30-year loan with lower payments, you can only deduct the mortgage interest paid on the new loan for 15 years.

And, any equity debt incurred is subject to a limit of the amount of the existing debt plus $100,000. Say, for instance, that you bought your house 10 years ago and have seen the property grow in value from $70,000 to $230,000. If you refinance your mortgage (on which you now owe $50,000), you may only deduct the interest paid on the total of your acquisition indebtedness in the property ($50,000) plus $100,000. You will be able to deduct the interest paid on $150,000.

Just be sure you keep your closing statement to show the IRS the points you paid, if any, to refinance the loan on your property.

Second mortgages

A second mortgage allows the homeowner to cash in on some of the equity that has built up in the home over time. Some lenders call a second mortgage a "junior lien". Getting a second mortgage is very much like taking out your first mortgage (i.e. you will be required to pay closing costs of 3-6% of the loan value).

You may deduct the interest paid on second mortgages made on or after October 13, 1987, up to the $100,000 limit had already been reached when the first mortgage was taken out. The amount of second mortgages made before that date is part of your acquisition indebtedness total figure. This means that if you had $50,000 left on your first mortgage as of that date, and had taken out a $ 25,000-second mortgage on the property prior to October 14, 1987, you would have an acquisition indebtedness of $75,000.

Home equity lines of credit (HELOC)

Where the traditional second mortgage gives the homeowner money in one lump sum, the home equity line of credit (HELOC) allows homeowners to use the equity in their home as a giant credit card. The lender allows the homeowner to borrow — at will — against the equity in the home, and charges interest only on the portion of the equity borrowed against. Therefore, your interest deductions for a home equity line of credit depending on whether you borrow against the equity during that year.

Curious about comparable options to access home equity? Learn more about a cash-out refinance!

The bottom line

Changes to the mortgage interest deduction and property tax deductions may not be all that impactful to you. According to Fortune.com, non-metropolitan areas make it generally easy to buy a home with a mortgage of less than $500,000 and continue to reap the tax benefits of using the mortgage interest deduction. But if you’re looking in expensive metropolitan areas ranging from Austin to Boston and all big cities in between, finding a home under $500,000 may be difficult.