Getting a Mortgage When Self Employed: The Complete Guide

Key Takeaways

- Qualifying for Traditional Mortgages: Self-employed entrepreneurs and freelancers can qualify for standard 15- and 30-year FHA, VA, and conventional loans by providing comprehensive income verification, typically requiring two years of tax returns, 1099s, and profit and loss (P&L) statements.

- Strategies to Boost Approval Odds: Borrowers can offset high debt-to-income (DTI) ratios caused by business write-offs by making a larger down payment, improving their credit score, paying off outstanding credit accounts, and demonstrating a stable self-employment history.

- Specialized Bank Statement Loans: For self-employed buyers seeking alternative documentation, the Bank Statement Loan Program allows qualification without tax returns, featuring a maximum 50% DTI, a minimum 600 credit score, and no private mortgage insurance (PMI) requirements.

- Alternative Low-Doc Mortgage Options: Borrowers can also leverage reduced-documentation programs like Stated Income/Stated Asset (SISA) or No Documentation (No Doc) loans, which trade strict income verification for higher down payments and excellent credit history requirements.

Trying to qualify for a mortgage even though you're concerned with your self-employment work history? We get it. It can feel like the mortgage process is geared more toward W-2 employees than self-employed entrepreneurs such as yourself. The key here is being able to verify your income to lenders, so they know you’re not high risk. You will have to take extra steps to reassure lenders, but it’s worth it. Despite the additional steps to verify your self-employed income, you can still qualify for the same mortgage programs as anyone else. Including popular programs like FHA, VA, and Conventional 15 and 30-year mortgages.

Here’s what to know if you’re looking for a home loan as a self-employed borrower.

Gather and fill out the right paperwork

The mortgage process is very well known for involving a lot of paperwork. Lenders need the total financial picture of mortgage applicants to get started. If you’re self-employed, you’ll typically need to gather details of at least two years’ worth of your entire financial history.

-

Federal tax returns

-

List of debts

-

List of assets

For business owners specifically, you may also need a profit and loss statement or a 1099 form.

Look more attractive to self-employed mortgage lenders

If you’re confident that you’re ready to become a homeowner, then go the extra mile to increase your chances of getting a home loan. One thing to keep in mind here is that not all lenders offer mortgages for self-employed borrowers. And the ones that do will want to know that you're serious about the process.

Improve your credit score

The higher your credit score is, the more attractive you’ll look to lenders, and you’ll qualify for a lower interest rate. A lower rate could save you thousands so look into improving your credit score.

Offer a large down payment

Lenders will see you as less of a risk if you have a more substantial down payment towards your home because they know you’ll be less likely to walk away from that equity. This is a common approach for a self-employed borrower as debt-to-income ratios are typically higher from being allowed to write off more resulting in a lower income. This can be offset by a making a more substantial down payment and waiting a few years to refinance out of the original loan into a lower interest rate.

Pay off credit accounts

The fewer monthly debt payments you have going into the mortgage process, the more cash flow you’ll have available to make your mortgage payments. You could even qualify for a higher loan amount if you pay off credit accounts, so it’s worth looking into.

Have a strong self-employment history

The longer the self-employment history you have and can prove, the more likely lenders will work with you. There’s typically two schools of thought when it comes to showcasing your track record. One is to start the mortgage process when you have at least two years' worth of history or more. The second school of thought is when interest rates are low, you should try to get a mortgage as soon as you’re ready, even if you don’t have a long history of stellar self-employment.

Be willing to provide more documentation

Being ready to fully document your income through previous years' tax returns, profit and loss statements, balance sheets and other income verification docs will improve your chances of qualifying for a home loan. You may also have to provide a business license depending on your underwriter, so it’s best to put your best foot forward and have these documents prepared beforehand.

Available self-employed mortgage options

There are a variety of loan programs that self-employed home buyers can qualify for that are also offered to self-employed buyers. Your financial situation determines which loan option is best for you, but certain loan types could be potentially more beneficial than traditional programs like FHA and Conventional.

Bank Statement Loan Program

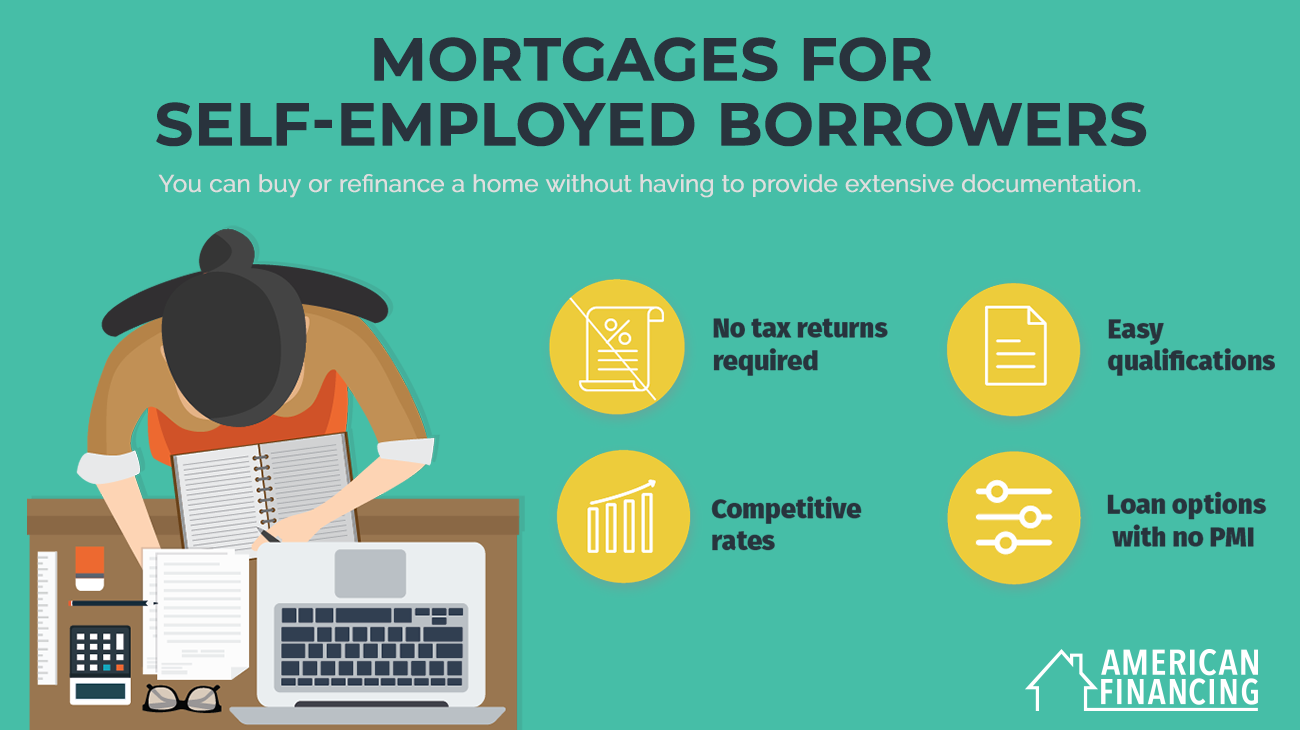

At American Financing, we have a flexible loan option made specifically for entrepreneurs, freelancers, small business owners, and self-employed borrowers. The bank statement mortgage can help you buy or refinance a home without having to provide tax returns and extensive documentation. They're easy to qualify with a maximum debt-to-income ratio (DTI) of 50%, a minimum credit score of 600, and best of all there's no private mortgage insurance (PMI) to pay. It makes affordable homeownership possible. Entrepreneurs, take advantage of this home loan today.

Stated Income/Stated Asset Mortgage (SISA)

“A type of reduced documentation mortgage program which allows the borrower to state on the loan application what their income and assets are without verification by the lender; however, the source of the income is still verified.”

No Documentation Loan (No Doc Loan)

“A type of reduced-documentation-required mortgage program in which income and assets aren't disclosed on the loan application and employment isn't verified. However, a credit check is typically required as lenders are counting on the fact that the borrower has a good credit history. No doc mortgages usually fall into the Alt-A classification, and tend to carry a higher interest rate and require a higher down-payment than a prime mortgage.”

For more information

Don’t let anyone tell you that you’ll never get a mortgage if you’re self-employed. Apply your business experience toward purchasing a home by educating yourself on the process, paperwork, and resources needed to make you stand out to mortgage lenders. There are also a variety of online resources to start you on your homeownership journey. For more information on mortgage options for self-employed owners or to learn how to qualify, contact the mortgage experts at American Financing.